Good Tech Companies Make Bad Bailout Targets

One month into Coronavirus-induced sheltering-in-place, America still lacks a clear plan to reopen the country. It’s increasingly apparent that the $2 trillion relief package passed by Congress in March will not be enough to prevent mass economic devastation, so discussions are underway to inject more money into the economy.

Naturally, this is a contentious topic. Lingering resentment about the 2008 TARP bank bailouts fueled populist movements throughout the 2010s. Among policymakers, “bailout” is still a dirty word.

One preferred populist solution to prop up the economy is to have the Treasury take equity stakes in businesses in exchange for bailout funds. This would protect workers by keeping existing businesses largely intact, but greatly diminish the positions of existing equity holders.

That approach sounds like smart politics, but it has been largely rejected by many corporate executives who are intent on preserving shareholder value, such as Boeing’s new CEO. On the other hand, some of the most forceful proponents of the wipe-out-the-shareholders philosophy are the prominent venture capitalists Bill Gurley and Chamath Palihapitiya.

Honestly, I was surprised to see them take that position, mostly because “venture capitalist” roughly translates to “professional shareholder.” Based on their long Twitter histories, there’s no reason to doubt their sincerity. That makes it especially striking, because it seems to be against their own self-interest.

But on closer examination, this might not actually be the case. That’s because most VC-backed tech companies seem to now have one thing in common: they tend to make bad candidates for government bailouts.

One reason why software companies are such attractive investments is their high margins: Facebook’s gross margin in December 2019 was 83%. General Electric, a great company from an earlier generation of American capitalism, had a gross margin of just 17.63%.

Based on current stock prices, Facebook is worth $540 billion, while GE is worth $54 billion. In other words, Facebook is worth ten GEs. However, that scale isn’t reflected in their employee count. While GE employs over 200,000 people, Facebook employs a relatively paltry 45,000. For every additional aircraft engine sold, GE needs to hire more factory workers, while the marginal cost of serving another Facebook ad is effectively zero. For investors covering fixed R&D costs, Facebook is clearly the more appealing option.

The differences in job-to-valuation ratios is even more pronounced at earlier stage tech companies: Notion, a hot productivity startup recently valued at $2 billion, currently just has 50 employees. At the other extreme we have Sanmina, a contract manufacturer employing 43,000 people, which is currently valued at $1.88 billion. Tech companies are richly valued not in spite of employing so few people, but because of it.

Nowhere is this truer than “tech-enabled” businesses such as Uber, Bill Gurley’s most famous investment. Although JP Morgan estimates that over 3 million people have participated in the gig economy, they were never actually employees. While this is good for Uber, who doesn’t have to pay drivers while demand for rides is down 70%, a huge number of drivers now lack income. This is all without Uber laying off a single person!

These are not perfect comparisons: Sanmina and GE are mature companies with stable or declining revenues, while Facebook and Notion both are expecting strong growth in the future. But for politicians whose main incentive is to preserve jobs in order to stave off mass unemployment and social unrest, it’s obvious that propping up technology companies isn’t the most efficient use of taxpayer money. So, Gurley and Palihapitiya are free to advocate for bankruptcies without perceptible harm to their portfolios.

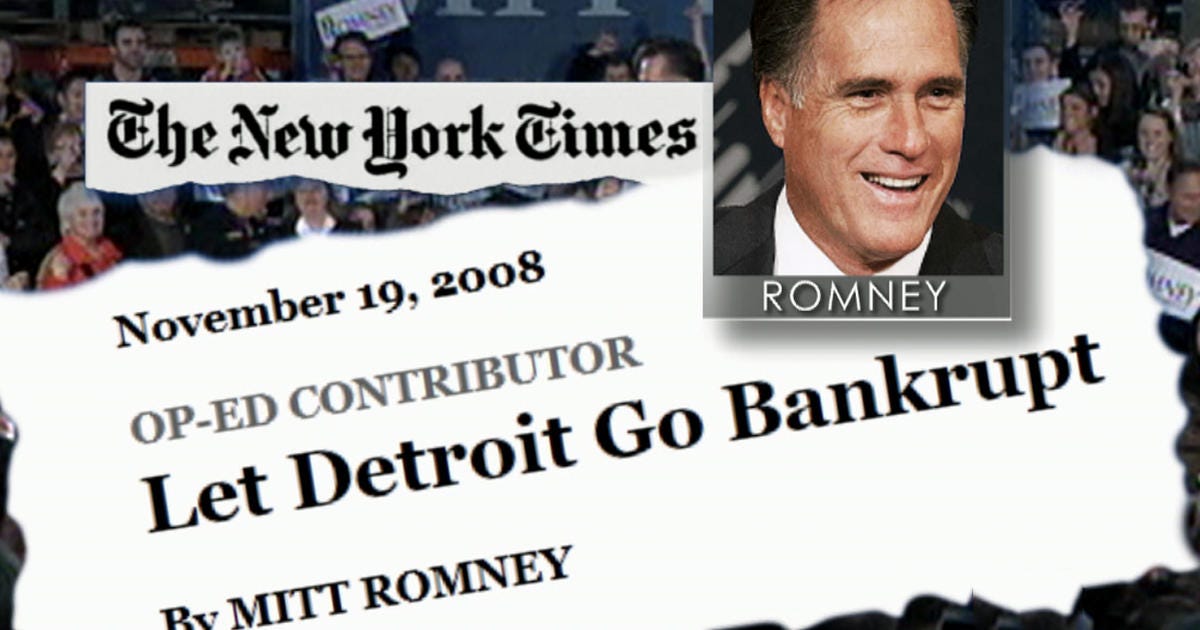

Frank Borman, the former chairman of Eastern Air Lines famously said that “Captalism without bankruptcy is like Christianity without hell.” While preserving the livelihoods of workers during a crisis should be a top priority for governments, Gurley and Palihapitiya are correct in claiming that bailouts oftentimes act as politically-driven redistributions of wealth that do not meet their stated goals. At the very least, they’re in good company: